Getting the right kitchen gear is a total game-changer, but let's be real—the upfront cost can stop any Los Angeles restaurant dead in its tracks. It doesn't matter if you're launching a new Los Angeles food truck, upgrading an established Mexican food spot, or opening a new Los Angeles pizza place; that price tag is a hurdle. Financing your restaurant equipment is a smart move that protects your cash flow while letting you get your hands on essential, brand-new gear. Think of it as a strategic investment in efficiency, reliability, and future growth.

Equipping Your LA Restaurant Without Draining Your Capital

Launching or upgrading a restaurant in the cutthroat Los Angeles food scene takes a serious investment, especially when you start looking at the kitchen. Outfitting a new Los Angeles pizza joint or a bustling food truck with commercial-grade ovens, refrigeration, and prep tables can easily eat up the biggest chunk of your budget.

Sure, paying cash might seem like the simplest way to go. But doing that often ties up the critical funds you need for payroll, inventory, and marketing—the stuff that keeps the lights on. This is exactly where strategic financing becomes your most powerful tool.

By choosing to finance, you can get the high-quality, warranty-backed equipment you need right now with predictable monthly payments. This approach helps you sidestep the risks and repair nightmares that often come with buying used gear, making sure your kitchen runs like a well-oiled machine from day one. You hang onto your capital for daily operations while your new, efficient equipment starts making you money immediately.

The Growing Demand for Modern Kitchens

The push for better equipment isn’t just a local trend. The global restaurant equipment market is absolutely booming, projected to jump from USD 4.8 billion in 2025 to a staggering USD 10.2 billion by 2035. This explosive growth signals a clear industry-wide shift as operators invest in better gear to meet rising customer demands for quality and speed.

For a complete picture of where your money goes, check out our comprehensive restaurant startup costs breakdown.

This strategic investment protects your most valuable asset: your working capital. Instead of a massive upfront expense, financing turns a large capital purchase into a predictable operating cost, making financial planning far more manageable.

Navigating Your Equipment Financing Options

Deciding to finance new restaurant equipment isn't just about picking a payment plan. It's a strategic move that needs to fit your business like a glove. Whether you're running a bustling Mexican food spot in East LA or a nimble Los Angeles pizza food truck, understanding your options is the key to making a smart investment.

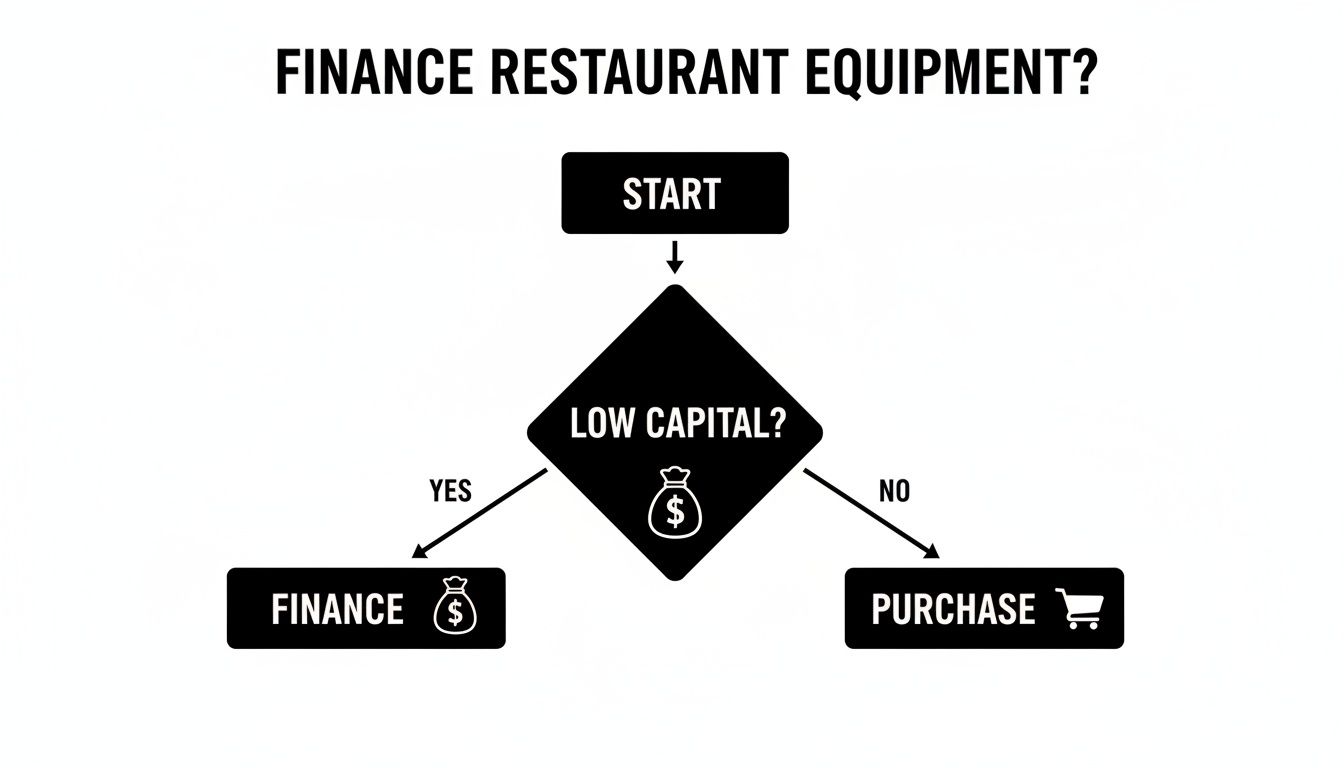

For most owners, the choice to finance comes down to one thing: protecting working capital. Cash is king, and tying it all up in equipment can be a risky play. This flowchart pretty much sums up the initial thought process.

As you can see, if capital is tight, financing gives you a direct path to getting the gear you need without draining your bank account.

Exploring the Four Main Financing Paths

Every financing route has its own pros and cons, making each one a better fit for different situations. Let's break down the most common choices for restaurant owners in LA and Orange County.

-

Traditional Equipment Loans: This is the most straightforward option. You borrow a lump sum to buy the equipment, and it's yours from day one. You build equity with each fixed monthly payment. This is perfect for foundational, long-lasting gear like a commercial range or a walk-in cooler. A new Mexican food restaurant, for example, would almost certainly use a loan for its core cooking line, knowing that equipment will last them a decade or more.

-

Equipment Leasing: Think of this as a long-term rental. You make lower monthly payments to use the equipment for a set period, like 36 months. When the term is up, you often have the option to buy it, renew the lease, or upgrade to a newer model. Leasing is a fantastic strategy for tech that evolves quickly, like POS systems, or for specialty items you're not ready to commit to. For a mobile Los Angeles pizza pop-up that needs to stay agile, leasing an oven keeps them competitive without the huge upfront cost. For a deeper dive, comparing coffee machine leasing vs buying is a great way to see the nuances.

-

Merchant Cash Advance (MCA): An MCA isn't technically a loan. It's an advance on your future credit card sales. A lender gives you cash upfront, and in return, they take a small percentage of your daily sales until the advance is paid back. It’s incredibly fast and easy to qualify for, making it a lifesaver for one of the many Los Angeles food trucks that suddenly needs a new freezer to avoid losing thousands in inventory. That convenience, however, usually comes at a much higher cost.

-

Vendor or Supplier Financing: Many commercial kitchen equipment suppliers, including us, partner with lenders to offer financing right at the point of sale. This really simplifies the whole process. You're working with a team that knows the equipment inside and out and understands its real value, which can make approvals much smoother.

This push to finance and equip modern kitchens is part of a huge industry trend. The North American market for commercial kitchen equipment is projected to grow by USD 41.81 billion, with a 7.4% CAGR from 2024-2029, all driven by a dynamic and ever-growing foodservice sector.

How to Prepare a Winning Financing Application

A strong application is your golden ticket. It's what gets you better financing rates and a much smoother approval process. When you get right down to it, lenders are just trying to answer one question: can you reliably pay this back? The best way to give them a confident "yes" is to be over-prepared with organized, professional documents.

Think of your application as the story of your business. It doesn't matter if you're a Los Angeles food truck, a new Mexican food restaurant in Orange County, or an established pizzeria—your paperwork has to paint a clear picture of your financial health and where you're headed. This isn't just about crunching numbers; it's about proving you have a solid plan.

Gathering Your Essential Documents

Before you even think about filling out forms, get your key documents together. Having these ready to go shows you’re organized and serious about your request to finance restaurant equipment.

- Business Plan: This doesn't need to be a 50-page novel. A concise plan that outlines your concept, target market (especially if you're in the LA/OC area), and projected revenue is perfect. For a food truck, a one-page summary often does the trick.

- Financial Statements: If you're an existing business, be ready with your Profit & Loss (P&L) statements and balance sheets for the last one to two years. This is your track record.

- Tax Returns: Lenders will almost always ask for both personal and business tax returns. They give an official, third-party verified look at your financial history.

- Bank Statements: Most lenders want to see three to six months of recent business bank statements to get a feel for your cash flow and daily account balance.

For a top-tier financing application, diligent tracking business expenses is non-negotiable, especially for initial equipment purchases. Clean, organized records make it so much easier to generate the accurate financial statements lenders need to see.

What Lenders Are Really Looking For

Lenders are going to scrutinize these documents for signs of stability and potential for growth. They're assessing risk, pure and simple. A strong application will clearly show consistent revenue, responsible cash management, and a healthy profit margin.

For Los Angeles and Orange County businesses, having your local permits and licenses in order is another big plus. It shows you're compliant and ready to operate legally, which instantly reduces the lender's perceived risk.

The goal is to present a complete and compelling case. Lenders are more likely to approve—and offer better terms to—an applicant who provides all necessary information upfront, making their job easier and proving you're a low-risk partner.

At the end of the day, a well-prepared application saves everyone time. It speeds up the review process and positions your restaurant, bar, or food truck as a professional operation worthy of investment. Whether you're financing a single refrigeration unit or outfitting an entire ghost kitchen, this prep work is your first step toward success.

From Application to Approval: What Happens Next?

You’ve done the legwork, gathered your documents, and hit "submit" on your financing application. So, what happens now? This is where the process really kicks into gear, and understanding the journey from submission to funding can take a lot of the mystery out of it.

The second your application lands in the lender's system, their underwriting team starts digging in. They'll typically pull your credit first, then move on to a thorough review of the documents you sent over. They're essentially verifying your financial story, looking for the stability and cash flow to comfortably handle the new payments.

Unpacking the Approval Timeline

You might be surprised at how quickly things can move, especially if your application package is complete and organized from the get-go. While every lender is a bit different, the path is usually pretty predictable.

- Initial Review (24-48 Hours): Most lenders get back to you with a preliminary decision within one to two business days. Think of this as a conditional green light, pending the final verification of all your info.

- Document Verification & Underwriting (1-3 Business Days): This is the deep dive. Underwriters will cross-reference your bank statements with your tax returns and business plan to make sure everything lines up. If they have questions, this is when they’ll reach out—responding quickly is the key to keeping the process on track.

- Final Approval & Contract (1 Business Day): Once underwriting gives the final okay, you'll receive the official approval and the financing agreement. This is the document that lays out all the terms, from the interest rate to the payment schedule. Read it over carefully before you sign.

A little insider tip: working directly with a supplier’s financing partners, like ours, often speeds things up. These lenders live and breathe the restaurant industry. They know the equipment, they understand the business, and that familiarity can make for a much smoother, faster approval.

Don't sweat it if a lender asks for more information. It’s a totally normal part of the process and a good sign that they're seriously considering your application. Just give them clear, prompt answers to keep things moving.

Seeing What Your Payments Could Look Like

Let's make this real. Imagine you're a food truck owner in Los Angeles and you desperately need a new commercial freezer and a stainless steel prep table. The total cost comes out to $10,000.

Example Payment Scenario:

- Total Equipment Cost: $10,000

- Financing Term: 36 months (a very common term for this amount)

- Estimated Monthly Payment: Roughly $320 - $380

Suddenly, that massive one-time expense becomes a predictable, manageable monthly operating cost. Instead of wiping out your cash reserves, you have a payment that fits right into your budget.

This is how you get the gear you need to grow—whether you’re launching a new Los Angeles pizza place or expanding your Mexican food pop-up—without putting your financial stability at risk. Breaking the numbers down like this makes the whole idea of financing much less intimidating and a lot easier to plan for.

Insider Tips to Improve Your Approval Odds

Getting a “yes” on a financing application is one thing. Getting a great deal that actually works for your business? That's the real win. Lenders are ultimately looking for stability and a solid plan, and a few smart moves on your end can dramatically improve your odds and put you in a much stronger negotiating position.

Here are the kind of insider tips that separate the successful applications from the ones that get buried in the pile.

First off, take a hard, honest look at your personal credit score before you even think about applying. If it’s not where you want it to be, take a few months to pay down some balances and make every single payment on time. It's amazing how a few points on your score can translate into a lower interest rate, saving you thousands over the life of the loan.

Next up, think about a down payment. I know, many financing options advertise little to no money down, and that can be tempting. But putting 10-20% down shows the lender you've got skin in the game. It’s a powerful signal that you’re serious and confident. This simple step reduces their risk, which in turn can significantly boost your approval chances.

Position Your Business for Success

Beyond the black-and-white numbers, the story you tell about your restaurant really matters. Lenders want to see a clear path to making money, and your personal experience is a huge part of that story.

-

Highlight Your Industry Experience: Maybe your restaurant is brand new, but you aren't. Be sure to showcase your years of experience as a chef, a manager, or even a food truck operator. This tells lenders you understand the tough-as-nails Los Angeles food scene and have what it takes to thrive.

-

Choose New, Warrantied Equipment: This one is big. Lenders see new equipment backed by a warranty as a much safer bet than used gear. When you choose new equipment from a trusted local dealer like us, you're not just buying a machine; you're strengthening your application with a reliable, long-term asset. You also get to dodge the maintenance nightmares and unexpected downtime that often come with used equipment.

This is especially true for the workhorses of your kitchen. Cooking equipment actually dominates the market, pulling in a massive 32.7% revenue share. And with North America accounting for 42% of a market projected to hit USD 46.12 billion in 2025, U.S. restaurant owners have a huge stake in outfitting their kitchens with gear they can count on. You can discover more insights about these food service equipment trends right here.

Shop Smart for Financing

When you're ready to see what rates you can get, be strategic. Don't just start firing off applications to every lender you can find online. Each one can trigger a hard inquiry that dings your credit score. Instead, work with a supplier who has a network of financing partners. They can often shop your application to several lenders with just a single, soft credit pull.

A common mistake I see is operators getting desperate and shotgunning applications everywhere. A focused, well-prepared approach with one or two strong lenders is far more effective—and it protects your credit score in the process.

When you bring together a strong personal financial picture and a compelling business case, you’re not just asking for a loan. You're presenting a solid investment opportunity. This proactive approach will help you get the funds you need to finance your restaurant equipment and get back to building a killer business.

Your Next Steps Toward a Fully Equipped Kitchen

Taking the plunge to finance restaurant equipment is one of the smartest strategic moves any Los Angeles food business can make when you're ready to grow. It doesn't matter if you're running a Los Angeles food truck, a bustling pizzeria, or a beloved local Mexican food restaurant—financing protects your cash flow while getting you the tools you absolutely need to succeed.

Opting for new, warranty-backed equipment is a solid investment in your kitchen’s future, guaranteeing both reliability and better energy efficiency from day one. When you partner with a local supplier right here in Southern California, you get direct pricing and incredibly fast shipping, often within just one or two business days. That combination brings total peace of mind and gets your kitchen up and running faster.

The right equipment is the foundation of your business. Financing it is the smart way to build a stronger, more resilient operation without draining your capital.

Ready to build a better kitchen? Our team is on standby to help you track down the perfect gear and map out a financing plan that actually fits your budget. For an excellent starting point, grab our detailed commercial kitchen equipment checklist to figure out exactly what you need.

Feel free to explore our equipment online or contact a representative today for a no-obligation quote and some personalized guidance.

We Get These Questions All The Time

Navigating the world of equipment financing can feel like a maze. To help clear things up, here are some quick, straightforward answers to the questions we hear most often from restaurant owners across Los Angeles and Orange County.

Can I Finance Restaurant Equipment With Bad Credit?

Yes, you absolutely can. It's a common misconception that bad credit is an automatic "no." The reality is your options might just look a little different, and maybe come with higher costs.

When a credit score is on the lower side, lenders just want to see strength in other areas of your application. Think of things like a solid history of recent sales, a willingness to put more money down upfront, or even just having years of experience in the industry.

For those with less-than-perfect credit, a few financing routes tend to be more welcoming:

- Merchant Cash Advances (MCAs): These are great because they're based on your future sales, not a number from a credit bureau.

- Specialized Leasing Programs: These often focus more on the value of the equipment you're getting rather than your personal credit history.

This is where working with a local supplier who has a network of financing partners really pays off. We can shop your application around to find a lender who gets your situation and is flexible enough to work with you.

Is It Better To Lease Or Buy Restaurant Equipment?

This is the classic debate, and honestly, it all boils down to your specific business goals and what kind of equipment you're eyeing. There’s no single right answer, but here’s how we help LA-area restaurants think through it.

Buying (usually through a loan) is a fantastic move for the workhorses of your kitchen—the foundational, long-lasting gear like a commercial range or a walk-in cooler. You build equity with every single payment, and eventually, that asset is all yours. For an established Mexican food joint, buying its core cooking line is almost always the best long-term play.

On the other hand, Leasing is perfect for equipment that evolves quickly (think POS systems) or when you just want to keep your monthly cash outflow as low as possible. If you're running a Los Angeles food truck and might want to pivot your menu down the line, leasing a specialized item like a pizza oven gives you that flexibility without a huge financial commitment.

How Quickly Can I Get Approved For Equipment Financing?

You might be surprised. The approval timeline can be incredibly fast—we often see approvals come through in just 24-48 hours. The key is having all your necessary documents ready to go and organized ahead of time.

Once you have the financing locked in, the next step is getting the actual equipment. This is a huge advantage of partnering with a local supplier. Because we have in-state warehousing, your new gear can be delivered to your restaurant in Los Angeles or Orange County in just one or two business days.

That quick turnaround from application to delivery is a game-changer. It means you can get your kitchen up and running—and making money—almost immediately.

Ready to equip your kitchen for success? The team at LA Restaurant Equipment is here to help you find the perfect gear and a financing plan that fits your budget. Explore our warehouse-direct pricing and get started today.