Launching a restaurant in Los Angeles is a high-stakes dream, but let's be honest: the massive upfront cost of a professional kitchen can feel more like a nightmare. This is where restaurant equipment financing comes in. It turns that paralyzing initial expense into a manageable, strategic investment.

Whether you're opening a new pizza place, a mobile food truck, or a classic Mexican restaurant, the right equipment is key. Financing allows your new oven or griddle to essentially start paying for itself over time, which frees up your precious cash for everything else you need to get off the ground.

Build Your Culinary Dream Without Draining Your Capital

Opening any kind of food spot in Southern California—whether it’s a bustling Mexican restaurant in East LA, a pizza shop in the Valley, or a nimble food truck cruising through Orange County—costs a lot of money to start. The heart of that investment is always the kitchen, and the price tag on commercial-grade restaurant equipment can stop a great concept dead in its tracks.

Financing isn't just a loan; it's one of the smartest tools in your toolbox.

Think of it as a strategic move for your future success. Instead of emptying your bank account on day one, you get all the essential gear you need while keeping a healthy cash reserve for:

- Inventory and Supplies: Buying the high-quality ingredients that make your menu special.

- Marketing and Grand Opening: Creating the buzz you need to pack the house from week one.

- Payroll and Staffing: Making sure you have a talented, reliable team ready to go.

- Unexpected Expenses: Having a financial cushion for the inevitable surprises that pop up.

A Smarter Path to Growth

This shift toward financing isn't just happening in SoCal; it's a major change in how restaurant owners everywhere think about big purchases. The equipment finance industry is on track to grow from USD 1,302.25 billion in 2024 to USD 1,437.04 billion in 2025.

That’s a huge jump, and it shows that smart operators are choosing manageable payment plans over risky, all-cash layouts. This kind of flexibility is a game-changer, especially for concepts like pop-up vendors, Los Angeles food trucks, and ghost kitchens that need to stay lean and agile to succeed.

Getting the right equipment is a huge first step, but you also have to protect your investment. As you build out your dream kitchen, don't overlook the importance of understanding liability insurance for contractors to shield your new business from the unexpected.

This guide will give you a clear roadmap for navigating your options, getting approved, and making the kind of financial decisions that will set your culinary dream up for success. But before we dive in, make sure you know exactly what you need with our complete commercial kitchen equipment checklist.

Choosing the Right Financing Path for Your Kitchen

Not every path to getting new equipment is the same, and what works for the new cafe down the street might not be the right fit for your established steakhouse. When it comes to restaurant equipment financing, the best choice really boils down to your specific business goals, how your cash flow looks, and what your vision is for the future.

For restaurant owners in the busy scenes of Los Angeles and Orange County, getting a handle on these options is the first, most crucial step.

Think of it like choosing a vehicle for a specific job. You wouldn't try to haul lumber in a sports car, right? And you definitely wouldn't fire up a semi-truck just to make a quick grocery run. Each financing option is a different kind of vehicle, built for a different purpose.

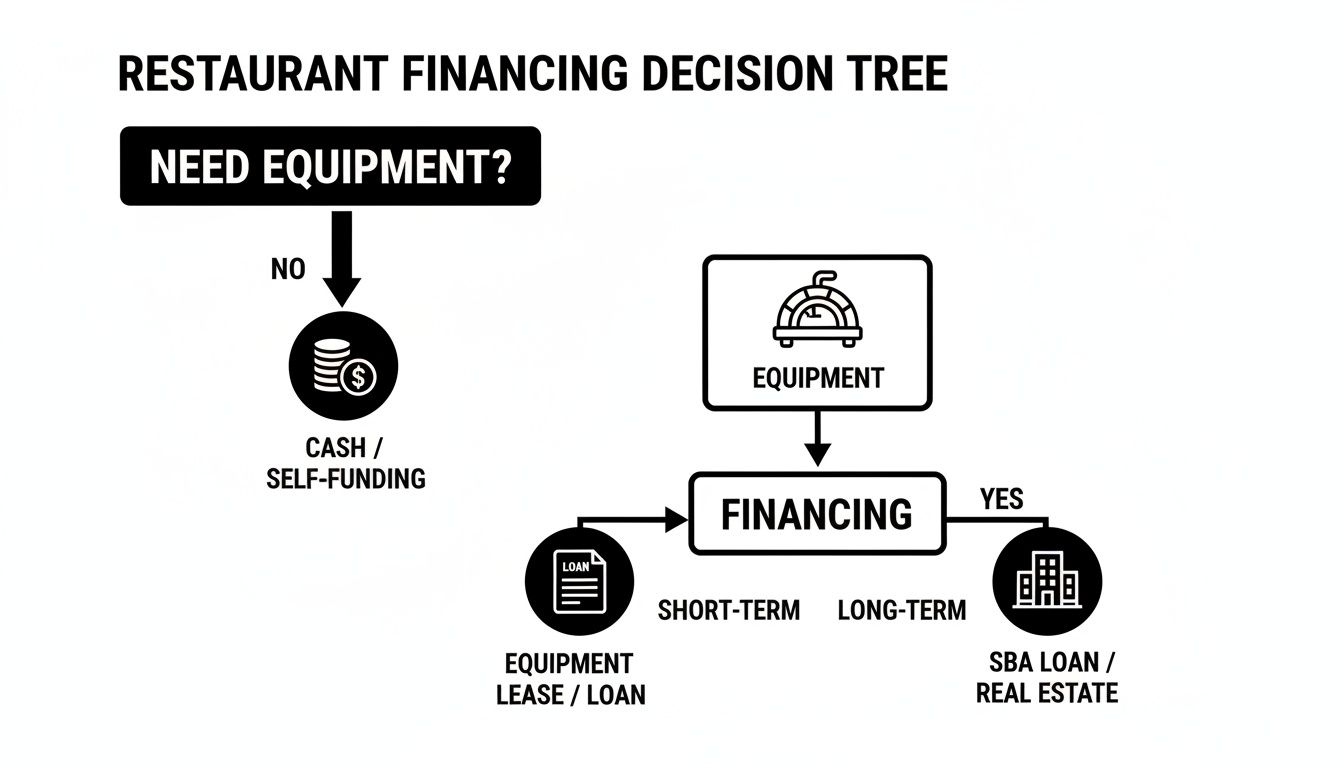

To get you started, here’s a simple way to visualize that first big decision: should you pay with cash you have on hand, or is it smarter to finance?

As you can see, once you decide that tying up your cash isn't the best move, a whole world of financing opens up. Let’s break down what each of those paths looks like.

Equipment Loans: The Direct Path to Ownership

This is the most straightforward route, and it works a lot like a car loan. You borrow a set amount of money to buy a specific piece of equipment—say, a brand-new pizza oven for your Los Angeles pizza joint—and pay it back in regular installments over a fixed period. Once that last payment is made, that oven is 100% yours.

- Who it’s for: Established restaurants that are buying core, long-lasting equipment they know they'll be using for years to come.

- The upside: You’re building equity in a valuable asset. Plus, the interest you pay is often a nice tax deduction.

- The downside: The monthly payments are usually higher than a lease, and you might need to put some money down upfront.

Equipment Leasing: The Flexible Rental Route

Leasing is a lot more like renting an apartment than buying a house. You pay a monthly fee to use an item, like a high-tech espresso machine, for a set amount of time. When the lease is up, you’ve got choices: you can return it, renew the lease, or in many cases, buy it out.

There are two main flavors of leases. Capital leases are more like a loan where you plan to buy the equipment at the end. Operating leases are true rentals, which are perfect for easily swapping out gear for the latest and greatest models when your term is up.

Operating leases are a fantastic choice for equipment that evolves quickly, like a POS system or that fancy specialty coffee brewer. If you're browsing for specific items, our guide on finding the best restaurant equipment for sale near me can help you see what’s out there.

SBA Loans: Government-Backed Power

Let's clear something up: the Small Business Administration (SBA) doesn't hand you the money directly. Instead, they guarantee a big chunk of a loan you get from a regular bank or lender. This makes the lender feel a lot safer, which means you often get better terms, lower interest rates, and more time to pay it back.

- SBA 7(a) Loans: This is the workhorse of SBA loans. It’s incredibly versatile and can be used for almost anything your business needs, including buying new equipment.

- SBA 504 Loans: These are for the big stuff. Think major fixed assets like real estate or a massive walk-in freezer system for a huge kitchen build-out.

The paperwork for an SBA loan can be a bit of a marathon, but the amazing terms make it a goal worth chasing for any qualifying business.

Business Lines of Credit: Your Financial Safety Net

Imagine having a credit card just for your restaurant. That’s pretty much what a business line of credit is. Instead of getting one big check, you’re approved for a pool of money you can dip into whenever you need it. The best part? You only pay interest on the cash you actually use.

It’s the perfect tool for those "uh-oh" moments, like when a freezer gives up the ghost on a hot July day. It’s also great for jumping on opportunities, like getting a steep discount for buying inventory in bulk. For the wild, unpredictable ride of the restaurant world, that kind of flexibility is priceless.

Merchant Cash Advances: Quick Cash with a Catch

A Merchant Cash Advance, or MCA, isn’t really a loan at all. A company gives you a lump sum of cash right now. In return, they take a cut of your future credit and debit card sales every single day until you've paid them back, plus their hefty fee.

While you can get money incredibly fast with almost no paperwork, it comes at a steep price. The effective interest rates can be sky-high. Think of this as the absolute last resort—an emergency option for when you need cash immediately and can't get approved for anything else.

What Does It Really Cost to Finance Your Kitchen?

It’s one thing to talk about loans and leases in the abstract, but let’s be honest—the only thing that really matters is how the numbers look on your budget. The true magic of restaurant equipment financing is how it takes a massive, scary price tag and breaks it down into a predictable monthly payment you can actually plan for.

To make this super clear, let’s ditch the theory and walk through a few real-world scenarios for popular restaurant concepts here in Los Angeles. These examples will show you exactly how a monthly payment gets calculated using the total cost, the loan term (how long you have to pay it off), and the interest rate.

Just remember, interest rates can swing quite a bit. Lenders usually save the best rates for established businesses with great credit, while newer spots or those with a shakier credit history might see higher numbers.

Scenario 1: Los Angeles Pizza Startup Package

Let's say you're about to launch the next great LA pizza joint. You need a solid deck oven, a heavy-duty mixer for that perfect dough, and a few stainless-steel prep tables to keep things moving. This is the core restaurant equipment that gets you from zero to serving amazing pies.

- Total Equipment Cost: $25,000

- Loan Term: 60 Months (5 years)

Here’s a quick look at how the monthly payment shakes out at different interest rates:

| Interest Rate | Estimated Monthly Payment |

|---|---|

| 8% | ~$507 |

| 12% | ~$556 |

| 16% | ~$608 |

For about $500 to $600 a month, you can get a fully kitted-out pizza kitchen ready for opening day without wiping out your startup capital. That leaves you with cash on hand for critical things like ingredients, marketing, and paying your new team.

Scenario 2: Los Angeles Food Trucks Equipment Kit

Food trucks are the heart and soul of the SoCal food scene, but their kitchens have to be ruthlessly efficient. For a new food truck specializing in Mexican food, you’re probably looking at a powerful flat-top griddle, a deep fryer for those crispy taquitos, and a refrigerated prep table.

- Total Equipment Cost: $15,000

- Loan Term: 48 Months (4 years)

Let's crunch the numbers for your new mobile kitchen:

| Interest Rate | Estimated Monthly Payment |

|---|---|

| 9% | ~$373 |

| 13% | ~$399 |

| 17% | ~$426 |

As you can see, getting your truck on the road could cost you less than $400 a month. It's a manageable payment that lets your new restaurant equipment start generating revenue and essentially pay for itself. If you want to dig deeper into startup expenses, check out our complete guide on restaurant startup costs.

Scenario 3: Mexican Restaurant Upgrade

Maybe you're running an established Mexican restaurant and need to keep up with the dinner rush. Upgrading to a high-capacity tortilla press and a larger range is more than just a purchase—it’s a direct investment in happier customers, faster service, and bigger daily sales.

- Total Equipment Cost: $18,000

- Loan Term: 36 Months (3 years)

An upgrade like this is a shorter-term play, so let's see how the financing works.

Think about it: a top-tier range can immediately boost your bottom line. If it helps you serve just 10 extra customers a day at $15 an order, that’s an extra $4,500 in revenue every month—more than enough to cover the financing.

Here’s the breakdown of what that new equipment would cost you monthly:

- With an 8% interest rate: You’re looking at a payment of about $565 per month.

- With a 12% interest rate: The payment nudges up to around $598 per month.

These examples prove that financing puts essential restaurant equipment within reach. Instead of staring at a price tag that feels impossible, you can see a simple, affordable line item for your budget. It gives you the confidence to build or upgrade the kitchen you've been dreaming of.

Your Step-by-Step Guide to Getting Approved

Applying for restaurant equipment financing can feel like the final hurdle in getting your kitchen up and running, but it doesn't have to be a nightmare. With the right preparation, you can turn a mountain of paperwork into a clear and compelling story about your restaurant's potential.

Think of your application as the business case for your loan. Every document you provide adds another layer of detail, painting a picture of a well-run operation with a bright future. Lenders are simply looking for stability, profitability, and a clear plan for how this new equipment will make you money.

A solid grasp of general business loan requirements is a great starting point. Having this foundational knowledge will make gathering your specific documents much more intuitive.

Your Essential Financing Application Checklist

Getting your documents in order before you even talk to a lender is the single best way to speed up the process. It's a pro move. Lenders love organized clients because it shows you’re serious and prepared.

Here's exactly what you need to have ready.

1. A Compelling Business Plan This is your restaurant's story. It needs to clearly outline your concept, who you're serving, your marketing strategy, and your financial projections. If you're already in business, highlight your wins and explain exactly how this new restaurant equipment fits into your growth plan.

2. Personal and Business Financial Statements These docs give a snapshot of your financial health. Be ready to provide:

- Profit & Loss (P&L) Statements: You'll typically need the last two years to show your revenue, costs, and—most importantly—profitability.

- Balance Sheets: These detail your assets, liabilities, and equity at a specific point in time.

- Recent Bank Statements: Lenders usually want to see the last three to six months of business bank statements to verify your cash flow.

3. Personal and Business Tax Returns Most lenders will ask for at least two years of both personal and business tax returns. This is how they verify the income you've reported and get a clear look at your financial history.

4. Official Equipment Quote You can't get a loan for a vague amount. You need a formal, itemized quote from a supplier like LA Restaurant Equipment. This document has to detail the specific make, model, and total cost of every single item you want to finance, from a walk-in freezer to a complete cooking line.

Telling a Powerful Financial Story

Your application isn't just a stack of papers; it's a narrative. Organize your documents to tell a story of growth and potential.

If your P&L shows a recent dip in profits, don't hide it. Include a brief, honest explanation—maybe you invested in a renovation that will pay off down the road. This kind of transparency builds trust and shows you have a firm handle on your business.

By presenting a complete and organized package, you demonstrate that you are a low-risk, high-potential investment for the lender. This single step can significantly improve your approval odds and even help you secure more favorable interest rates.

This preparation is more important than ever. The global restaurant equipment market is booming, projected to jump from USD 4.8 billion in 2025 to USD 10.2 billion by 2035.

Why the huge growth? Stricter food safety standards and a major push for energy efficiency are forcing operators to upgrade their gear. For restaurants right here in Los Angeles, financing modern equipment isn't just an option—it's a crucial step to stay compliant and competitive.

How to Secure the Best Possible Financing Rates

Getting approved for restaurant equipment financing is a huge step forward, but that’s really only half the battle. The next, and arguably more important, goal is to lock in the best possible terms—we’re talking lower interest rates, flexible payment schedules, and conditions that actually work for you.

Think of it this way: your approval gets you in the game, but your rate determines how you win. A lower interest rate doesn't just mean a smaller monthly payment. Over the life of a loan, even a one or two percent difference can save you thousands of dollars, freeing up that cash for inventory, marketing, or your next big growth project. The good news? You have more control over this than you think.

Strengthen Your Credit Profile

Before you even think about filling out an application, you need to know exactly where you stand with your credit. Lenders are going to pull both your personal and business credit scores to get a feel for your financial reliability. A higher score tells them you’re a low-risk borrower, which almost always translates to a better interest rate.

Here’s how to polish up your credit before you apply:

- Check for Errors: Pull reports from all the major credit bureaus. Go through them with a fine-tooth comb and dispute any mistakes you find right away. A simple error could be costing you valuable points.

- Pay Down Balances: Zero in on reducing high-balance credit cards and other revolving debts. Lowering your credit utilization is one of the fastest ways to give your score a boost.

- Make On-Time Payments: Your payment history is the single most important factor. In the months leading up to your application, make it your mission to ensure every single bill is paid on time, every time.

Present a Rock-Solid Business Plan

Don't treat your business plan like a homework assignment—it’s your most powerful negotiation tool. A detailed, well-researched plan that projects clear profitability gives lenders the confidence they need to offer you their best terms. It proves you’ve done the work and have a clear path to generating the revenue needed to cover your payments and then some.

Your financial projections are the heart and soul of your business plan. Lenders need to see realistic, data-backed forecasts that prove the new restaurant equipment will directly contribute to your bottom line, essentially paying for itself over time.

A strong plan shows you’re not just buying a shiny new oven; you're making a strategic investment in the future growth of your restaurant.

Increase Your Down Payment

One of the most direct ways to snag a better rate is to come to the table with a larger down payment. From a lender’s perspective, a bigger down payment seriously reduces their risk. The more of your own money you put into the purchase, the less they stand to lose if things get tough.

This simple act of good faith often encourages lenders to reward you with a lower interest rate. Even bumping your down payment from 10% to 20% can make a noticeable difference in the terms you’re offered. It shows you have real skin in the game and are all-in on your restaurant’s success.

Work with an Experienced Equipment Supplier

Finally, don’t underestimate the power of who you know. Partnering with a supplier like LA Restaurant Equipment gives you an immediate advantage. We’ve spent years building strong relationships with a network of financing partners who specialize in the foodservice industry.

These lenders get the unique challenges and opportunities of running a restaurant here in Los Angeles. They understand the value of commercial-grade equipment and are often much more willing to offer competitive terms to our clients. Instead of cold-calling lenders on your own, you can tap into our network and connect with financiers who are already primed to say yes.

Partnering with LA Restaurant Equipment for Smarter Financing

Getting approved for a loan is just one piece of the puzzle. The other, arguably more important piece, is picking the right equipment partner to bring your vision to life. This is where your kitchen dreams meet your financial reality.

We're not just another supplier. Think of us as your partner, deeply invested in the success of Southern California’s incredible food scene—from the latest Los Angeles pizza joint to established Mexican food spots in Orange County.

Working with us takes the headache out of the whole process. Instead of juggling a dozen different quotes and financing applications, you get one streamlined solution. We’ve built strong relationships with trusted financing partners who actually get the restaurant business, which means you get access to competitive terms from lenders who know what you’re up against.

The LA Restaurant Equipment Advantage

Our entire business is set up to give you an edge. We’ve cut out the expensive showrooms and high-pressure sales commissions, which lets us offer warehouse-direct pricing on brand-new equipment that’s fully backed by warranties. You get top-tier, reliable gear without the crazy markup.

You also get your kitchen up and running way faster. We offer fast, free shipping on orders across California, and most of our deliveries land in just one to two business days. When a fryer goes down or you're trying to hit an opening date, that kind of speed is everything.

When you choose us, you're getting more than just equipment. You're getting the financial breathing room to grow, backed by a partner who delivers top-quality products and straightforward restaurant equipment financing built for SoCal operators.

The demand for modern, quality equipment isn't slowing down. The food service equipment market was valued at USD 40.04 billion in 2025 and is on track to hit USD 59.02 billion by 2032. While full-service restaurants are a huge part of that, the other 28%—quick-service joints, cafes, and Los Angeles food trucks—are innovating like crazy, and we’re right there with them.

You can see it in how manufacturers are stepping up their game, moving to full stainless-steel construction for better durability—the kind of quality you'll find throughout our catalog. If you're curious, you can explore more about these market trends and how they're shaping the industry.

Your Next Step to a Better Kitchen

Whether you're firing up a new pizza place in Los Angeles or giving your current kitchen a much-needed upgrade, our team is here to help you make it happen. We offer that perfect blend of high-quality equipment and smart financing to turn your goals into a reality.

Ready to build the kitchen you've always wanted?

- Explore Our Catalog: Browse our extensive selection of new commercial kitchen equipment online.

- Get a Personalized Quote: Contact our team for a detailed quote on the specific items you need.

- Receive Expert Financing Guidance: Let us connect you with our financing partners to find the best possible plan for your budget.

Common Questions About Restaurant Equipment Financing

Jumping into the world of restaurant equipment financing can feel like a lot, especially when your main focus is perfecting your menu for a new Los Angeles pizza place or giving your current kitchen a much-needed upgrade. We get it. Here are some of the most common questions we hear from SoCal restaurateurs, with straight-up answers to help you make your next move with confidence.

Can I Get Restaurant Equipment Financing with Bad Credit?

Yes, it’s absolutely possible. While a stellar credit score makes things easier, lenders know that business finances aren’t always a straight line. They’ll often look past the three-digit score to see the bigger picture of your business's health.

For example, a strong, steady cash flow, a good track record of being in business, and the value of the equipment itself (which secures the loan) can all make a huge difference in your favor.

A traditional bank loan might be a long shot, but that's where alternative financing really shines. Options like merchant cash advances or specialized leasing programs are built for business owners who don't have perfect credit. Our financing partners are pros at finding a way forward, no matter your situation.

Is Buying Used Equipment a Better Deal Than Financing New?

The low sticker price on used equipment is definitely tempting, but it’s a gamble that can come with some serious hidden costs. Used gear almost never includes a warranty, meaning you're on the hook for every single expensive repair that pops up—and they always seem to pop up at the worst times. Older models also guzzle more energy, which means higher utility bills month after month.

Financing new equipment with a full warranty gives you predictability and peace of mind. You get a modern, reliable machine that keeps your energy costs down, and your predictable monthly payment is a much smarter play than a surprise repair bill that could shut down your whole operation.

How Quickly Can I Get Approved for Equipment Financing?

The timeline really hinges on the type of financing you’re going for. Simple applications for smaller loans or equipment leases can often get the green light in as little as 24 to 48 hours.

On the other hand, something more involved like an SBA-backed loan can take several weeks to move through the pipeline because of all the detailed paperwork required.

The single best way to speed things up? Be prepared. Having all your documents from our application checklist organized and ready to go can shave a ton of time off the process, getting you the funds you need to get cooking much faster.

Can I Finance Equipment for a Food Truck or a New Restaurant Startup?

You bet. In fact, many lenders specialize in funding new businesses, including mobile kitchens like Los Angeles food trucks. They know that every great L.A. restaurant had to start somewhere.

For a brand-new venture, lenders will understandably lean more heavily on your personal credit score and the quality of your business plan. But because the shiny new equipment you’re buying serves as collateral, it takes a lot of the risk off their plate. This makes them much more open to working with entrepreneurs who are just firing up the grill for the first time. We’ve helped countless local food trucks and restaurant startups get the funding they needed to bring their vision to life.

Ready to find the perfect equipment and the right financing to match? At LA Restaurant Equipment, we provide top-quality, warranty-backed gear with flexible financing options designed for Southern California’s dynamic food scene. Explore our catalog and get a personalized quote today!